Structuring in Money Laundering

Many Anti-Money Laundering (AML) regulations don’t wait for crimes to happen. Instead, they require businesses to identify and prevent suspicious activities proactively, meaning an organization can be in violation simply for lacking adequate safeguards, regardless of whether money laundering actually occurred.

One such suspicious activity is structuring – a money laundering trick in which big sums are split into smaller transactions to dodge bank reporting rules. In this article, we’ll explain how structuring is related to smurfing (a type of structuring), why both practices are considered illegal, and how companies can protect themselves.

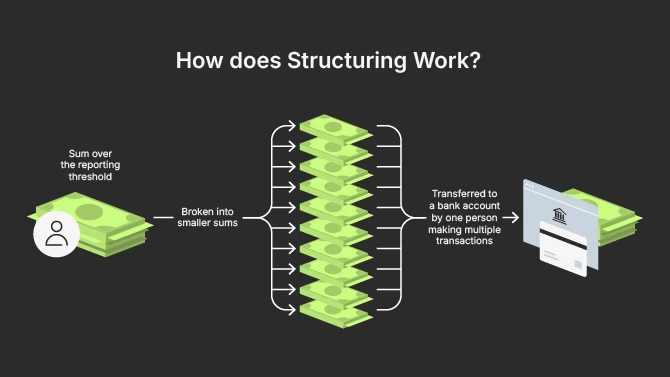

How Does Structuring Work?

On the surface, structuring is a simple money laundering method aimed to trick financial institutions. It involves dividing money transfers into many smaller increments. The purpose of structuring is to stay below the reporting thresholds set by financial institutions and regulatory authorities.

Here is how it works: transactions over $10,000 are often subject to reporting requirements, so by keeping each individual transaction below the reporting threshold, the money launderers aim to trick the financial institution and avoid detection.

Let’s take a look at some examples to better understand how structuring plays out in banking:

- Cash deposits just under reporting limits: A person deposits $9,900 cash multiple times over consecutive days in different branches to avoid the $10,000 Currency Transaction Report (CTR) requirement.

- Multiple accounts funnel: Funds are split across multiple bank accounts and later consolidated into a single „clean” account to disguise the source. For example, splitting $100k into $5k deposits across 20 accounts.

- Use of prepaid cards and money orders: Instead of direct deposits, criminals buy numerous prepaid cards or money orders in small amounts to evade detection. For example, buying multiple instruments under the $3,000 ID threshold.

- Crypto on- and off-ramping in small lots: Dividing large cryptocurrency transactions into smaller ones to bypass monitoring thresholds.

- Trade and merchant split invoicing: Dividing a large invoice into several smaller ones to move money without raising alarms. For example, breaking one $100k shipment into 10 × $10k invoices.

- Micro-structuring: Making dozens of tiny wire transfers – for example, $200 × 50.

The aim of these tactics is to bypass the early stages of the AML processes – particularly the „placement” and „layering” phases, where large suspicious cash flows typically trigger alerts.

In March 2020, Financial Industry Regulatory Authority (FINRA) brought proceedings against a financial advisor who was accused of structuring his personal bank transactions to avoid reporting requirements. He made multiple deposits of $9,000 and withdrawals of $6,500, deliberately keeping each transaction under the $10,000 reporting threshold. This case shows that structuring isn’t just done by criminals or cash-intensive businesses; but even regulated professionals can commit this offense. Source

The Consequences of Structuring

At its core, structuring is the practice of breaking up large financial transactions into smaller ones below reporting thresholds to avoid detection. The goal of structuring is to evade mandatory bank reporting rules designed to flag suspicious activities. Because of its role in helping criminals disguise dirty money, structuring is illegal and considered a significant AML red flag.

Why is structuring illegal? Put simply, it’s illegal because it deliberately thwarts financial transparency laws. In other words, structuring “intentionally avoids financial reporting thresholds set by law” and is often used to conceal illicit funds.

And the penalties are severe. Financial institutions that fail to detect or report structuring expose themselves to:

- Hefty fines imposed by regulators for AML failures.

- Loss of banking licenses or other operational restrictions.

- Criminal prosecution for individuals involved, including bank employees who knowingly facilitate structuring.

- Reputational damage that scares off partners and customers.

For example, in the US, structuring can lead to up to five years in federal prison and fines up to $250,000 for individuals. If linked to other crimes, penalties can double. It’s also important to note that structuring is illegal even if the money is legitimate.

Finally, let’s not forget about the social consequences of structuring, including allowing drug traffickers, smugglers, and other criminals to expand operations. Additionally, it transfers economic power from the market, government, and citizens to criminals.

Former US House Speaker Dennis Hastert structured $1.7 million in withdrawals to avoid reporting. In 2015, he was indicted and convicted, showing how seriously regulators treat structuring. He received a 15-month prison sentence and paid a $250,000 fine. Source

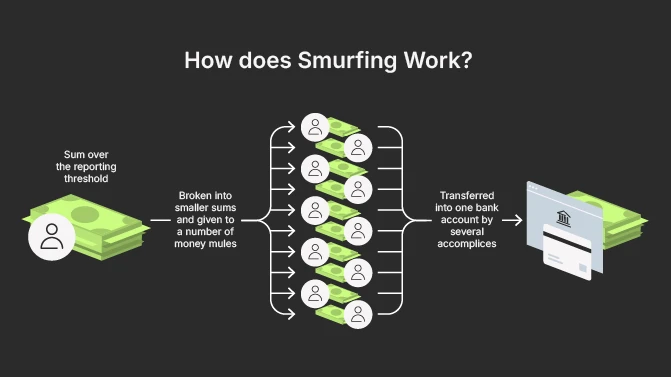

How Does Smurfing Work?

Smurfing is a form of structuring conducted by multiple individuals or „money mules” who coordinate to spread illicit funds across different accounts or financial institutions.

For example, a criminal organization might instruct dozens of people to deposit small sums below the reporting threshold at different branches or banks. Let’s say: ten people each deposit $9,000 at different banks on the same day, moving $90k total. These small deposits are then aggregated through a funnel account, making the money harder to trace.

Much like structuring, the purpose of smurfing is to stay below the reporting thresholds set by financial institutions and regulatory authorities. Additionally, smurfing may involve a chain of unusually complex transactions, with funds changing hands multiple times through multiple accounts and entities to further obscure the origin of the money. Because smurfing involves networks, it requires robust link analysis and behavioral analytics to detect.

The Birth of Smurfing

Alberto Barrera Duran, nicknamed „Papa Smurf”, pioneered the smurfing technique to launder drug money for Colombian cartels. He evaded detection by breaking large amounts of cash into smaller transactions, buying money orders and cashier’s checks in amounts below $10,000 to avoid mandatory bank reporting requirements. The scheme was dismantled in 1984 when Barrera and 13 others were charged with conspiracy to defraud the United States. While Barrera fled to Colombia, others were arrested and imprisoned. The operation’s success in exposing this loophole led directly to the 1986 Money Laundering Control Act, which made smurfing a specific federal crime. Source

Structuring vs. Smurfing

You might wonder – are structuring and smurfing the same? Though they’re closely related, they’re slightly different:

- Structuring is the act of splitting transactions to avoid reporting thresholds done by one person.

- Smurfing is structuring specifically done by a group or network of individuals (also called „smurfs”) who use multiple accounts or identities to scatter deposits or transactions.

Both are illegal because they aim to evade AML reporting rules designed to detect suspicious activity early. So, whether it’s one person breaking up transactions or many people coordinating across accounts, the law treats both practices as serious offenses. To detect and prosecute these illegal activities, regulators rely on banks submitting a formal report.

Filing a Suspicious Activity Report

In the United States, public deposits in banks and savings associations are insured by the Federal Deposit Insurance Corporation (FDIC), established under the Federal Deposit Insurance Act (FDIA). The FDIC and federal banking regulators have enforcement authority over insured depository institutions, supervising that all banks comply with AML laws and regulations.

Naturally, financial institutions are obligated to file a Suspicious Activity Report (SAR) if they believe a customer is manipulating transactions to evade reporting requirements. Almost any conduct that a bank finds suspicious can be covered by SARs.

First, the Financial Crimes Enforcement Network (FinCEN), which will look into the occurrence, must be informed. It is the duty of a financial institution to submit a report within 30 days, or, if more evidence needs to be gathered, an extension of up to 60 days may be requested. Importantly, the institution does not need to prove that a crime has been committed to submit SARs.

FinCEN requires that the SARs filed by financial institutions identify the following five elements:

- Who is conducting the suspicious activity?

- What instruments or mechanisms are being used?

- When did the suspicious activity take place?

- Where did it take place?

- Why does the filer think the activity is suspicious?

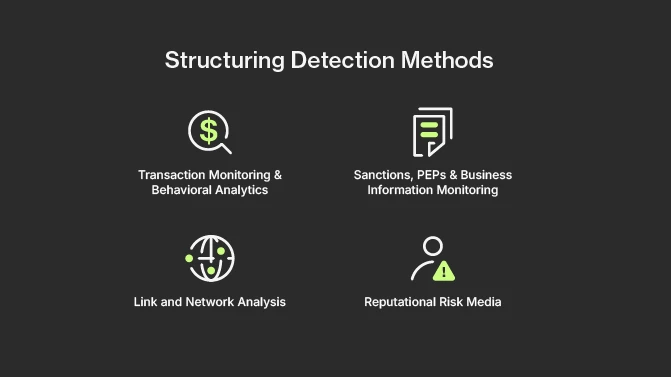

How Businesses Detect Structuring

Banks and financial firms deploy a range of AML controls against structuring. Here are some key detection methods:

Transaction Monitoring and Behavioral Analytics

These systems flag unusual transaction patterns such as:

- Frequent cash deposits just below reporting thresholds

For example, if a customer deposits $9,900 in cash every day at different branches to avoid triggering reports, the system will flag this as an unusual pattern of repeated deposits just under $10,000.

- Rapid deposits and withdrawals

For example, a client deposits large sums in the morning and withdraws most of it within a few hours multiple times a week – this will raise suspicion about the source and use of funds.

- Branch hopping (using multiple branches to split transactions)

For instance, a client makes multiple deposits of $5,000 at different branches in the same city on the same day, designed to bypass the single-branch reporting limit.

- Linked devices or IP addresses used to access different accounts

If two or more accounts are accessed frequently by the same IP address or device, this may indicate a structuring activity coordinated by one individual.

Some institutions use rule-based models with fixed thresholds, while others employ machine learning to spot nuanced patterns or velocity spikes that might indicate structuring.

Link and Network Analysis

By mapping connections between accounts, account holders, IP addresses, devices, or cryptocurrency wallets, banks identify smurfing networks and coordinated structuring efforts.

Bank analysts map a network showing multiple accounts all linked to a single owner’s phone number and IP address. These accounts receive various small deposits before funneling money into one main account, revealing a smurfing network.

For example, a criminal organization recruits multiple individuals (smurfs) to open bank accounts using their own names but linked to a single coordinator’s phone number and IP address. After each smurf makes small cash deposits below reporting thresholds at different branches, all of these funds are then transferred to a central account controlled by the coordinator. Banks can detect this scheme through network analysis by identifying the shared phone number, IP address, and the pattern of transfers converging into one funnel account.

Global Sanctions, PEPs, and Business Information Monitoring

Continuous screening against sanctions lists, PEP databases, and adverse media helps banks identify higher-risk customers potentially involved in illicit activities. For example, a screening tool flags that a customer was recently added to a sanctions list or identified as a politically exposed person, which then triggers enhanced scrutiny, aka enhanced due diligence protocol.

Reputational Risk Media

While adverse media screening specifically targets negative information linked to individual persons (like clients, beneficial owners, or PEPs) during customer due diligence, reputational risk media looks at any negative press, social media activity, or public controversies affecting the institution itself, its executives, or related parties that might damage reputation beyond just compliance risks.

Therefore, monitoring news and social media for negative headlines linked to customers or their associates is very important for bank’s risk management, as it helps protect their reputation and maintain trust with customers.

For example, a bank’s CEO is featured in news reports alleging involvement in a lawsuit or unethical behavior. Compliance teams receive alerts about this negative coverage and decide to increase monitoring of the bank’s activities and review governance procedures. In addition, they are also able to timely communicate with stakeholders, mitigating concerns and preventing reputational damage. Ondato’s AML monitoring solution offers a number of tools to ensure your clients are who they say they are.

Reporting and Regulatory Obligations

Providing the foundation for a safe and trustworthy financial system, reporting and regulatory obligations are crucial for banks if they want to limit their risks and protect customer funds.

The anti-money laundering and Know Your Customer (KYC) rules require banks to monitor and report suspicious activity, actively preventing financial crime like money laundering and the funding of illegal activities. Otherwise, financial institutions risk receiving massive fines, be subject to legal action, and lose their reputation.

Here are a few regulatory reports that financial institutions must adhere to:

- Currency Transaction Reports (CTR) are filed for cash transactions exceeding a certain threshold (commonly $10,000 in the US).

- Suspicious Activity Reports (SAR/STR) are submitted when there’s suspicion of structuring, even if transactions don’t exceed reporting thresholds.

AML reporting rules, and records keeping, vary across jurisdictions. As to the enforcement bodies: in the US, the Bank Secrecy Act (BSA) mandates these reporting requirements, while it’s the EU’s AML directives that imposes similar obligations in Europe. Yet the goal remains the same – to stop money laundering and related financial crimes early on.

Last Thoughts

Structuring is an illegal trick used to launder money by splitting large amounts into smaller transactions that fly under the radar of bank reporting requirements.

Even though structuring might sound somewhat harmless, it causes real damage; it helps criminals hide their profits, fuels corruption, and throws markets off balance. When these schemes go unchecked, they chip away at economic stability and erode public trust in the financial system.

From damaged reputation to huge fines and prison time, the consequences are quite serious for everyone involved. That’s why banks use sophisticated tools, such as transaction monitoring, network analysis, and continuous screening, to catch structuring and smurfing before they spread. By understanding and fighting structuring, we protect not just financial markets, but also the society that depends on them.

FAQ